This analysis shows baseline forecasts, on the expected performance, in the major economies of the region, as well as the risks and strengths, highly prized. by various experts, in a challenging global environment.

By Valora Analitik for Grupo SURA

Most Latin American economies grew below their potential in 2018, such as Colombia, Chile, and Mexico, while other political and social problems led to problematic economic consequences, for example in Argentina, Brazil, and Venezuela. Counted were those that remained stable, with outstanding growth, such as Peru, Panama, and the Dominican Republic.

Although the forecasts for 2019 are more favorable, and see a recovery against previous years, in its main economies, external risks have not disappeared, taking into account the impact of aspects such as trade tensions between the United States and China, volatility in the markets of capitals, and factors for and against domestic consumption of relevant countries, in the region.

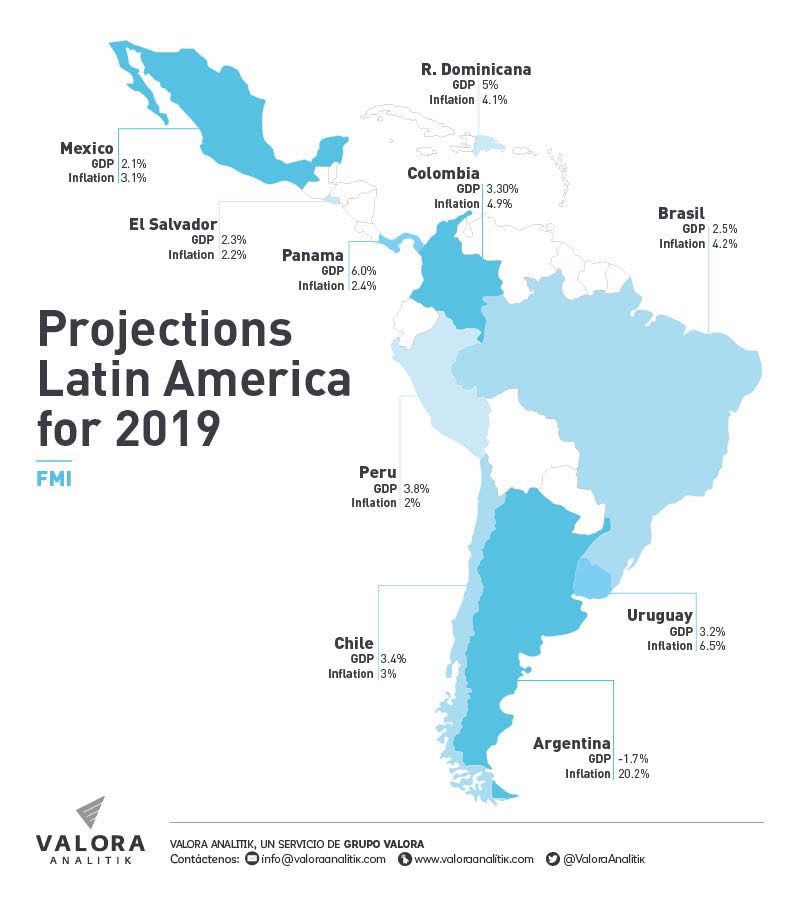

It is expected, that the gross domestic product (GDP) of the region will expand between 2% and 2.5%, this year, a modest growth compared to the 3.5% expected for the world economy, a projection in which the perspectives of the International Monetary Fund (IMF) and the Organization for Economic Cooperation and Development (OECD), coincide.

Growth and environment

In any event, without Argentina and Venezuela, the GDP growth in Latin America has been increasing at a moderate pace, marked "by the weakening of the world economy and the growth of political uncertainty, which contribute to the slowdown of the growth momentum," says the Director of the Western Hemisphere (FMI) Department, Alejandro Werner.

Regarding countries where SURA has a presence, IMF expects the greatest advances to occur in Colombia, Brazil, and Uruguay, as long as there is stability in Peru and Mexico, deceleration in Chile, and the recession in Argentina maintained, with signs of recovery. In other smaller economies, Panama will continue to lead growth, followed by the Dominican Republic and El Salvador, which will have stability.

"The best prospects for 2019, in the main Latin American economies, does not mean that the region is immune to what happens in the external environment," explains Cristobal Doberti, Manager of Regional Savings and Investments of SURA Asset Management.

The analyst points out, that the developed economies stem from a period of robust growth, and are now going through a slowdown, due to fiscal depletion and higher interest rates. In contrast, Latin America rose, from some complicated years, and is going through a recovery process, in its principal economies.

Among the external risks to the growth rate in Latin America, are the protectionist measures announced by several G20 Countries, which the IMF catalogs as the main threat for this year. From that perspective, tensions between the United States and China could be reflected in less trade, and the slowdown of the “Asian giant”.

In that scenario, the main impact for the region would be the decline in the prices of basic goods (commodities), according to Fitch Ratings Sovereign Ratings Analyst, Richard Francis.

If the Latin American economy is not homogeneous, a significant percentage of countries depend on commodities, as is in the case of Chile and Peru. "The focus is and will remain China's performance, during 2019, because it is the economy that generates dynamic sectors of basic commodities," adds and the Dean of Faculty of Economics and Business at the Universidad Santo Tomas de Chile, Guillermo Yánez.

Perspectives by countries

Brazil, Colombia, Peru, and Mexico had presidential successions, during 2018, for which the Head of Latin America, in the Development Center of the OECD, Sebastián Nieto, is optimistic, "because it is associated with the political capacity to present important structural reforms that are required."

With the exception of Mexico, there is appreciation that "changes in government have generated confidence in the business sector and will probably attract more investment," adds Richard Francis, Fitch Ratings Sovereign Ratings Analyst.

In the case of Brazil, the Analyst of SURA Asset Management said that the challenges come from the weakness of external accounts, and if there are no changes with social spending, "the situation may deteriorate in a significant way."

With regard to Mexico, Doberti said that it depends a great deal on what happens with the United States, and the uncertainty of the economic policy path of the new government, and what it may generate with International Investors and Business Leaders.

As for Colombia, the IMF sees signs of growth, still below potential, in support of monetary policy, the execution of the fourth-generation infrastructure program, and recent changes in tax policy, in favor of investment.

In the case of Argentina, the recession is expected to continue, but in a more contained manner.

According to the consensus of analysts surveyed by Focus Economics, the GDP would have a contraction of 0.9% and inflation would reach 29%, close to the Moody's projection of -0.8% and the expectation of an inflation rate of 32.80%.

Faced with the performance of other economies, the Head of Latin America in the OECD Development Center, pointed out the clear trend that Panama and the Dominican Republic will continue to be the countries with the highest growth, in the region. However, he commented that "we must examine the quality of that growth, for example, in the case of Panama, there are few sectors that grow well and mark the overall growth."

Aspects found in exchange matters

The behavior of Latin American currencies against the dollar is a bit more even, as both Francis and Yanez agree, that most of these are going to depreciate during 2019.

"In the long term, the dollar is overvalued, with respect to most of the region's currencies, except for the Brazilian Real (BRL), but we will experience frequent volatility bubbles, during the year, in which the dollar will rise and then return to its initial levels, associated to the least liquidity, in that currency," Yánez explained.

However, from the OECD, it is perceived that some countries converge towards stability, and does not foresee stronger movements, after the depreciations, in 2018.

Finally, Doberti said that local currencies are likely to suffer some depreciation, because Latin American economies are dependent on raw materials that relate to the business cycle. In this sense, for example, the Colombian Peso is closely linked to the volatility of oil prices.

In any case, the behavior of the dollar will depend, significantly, on the movements and the decisions made by the Federal Reserve of the United States (FED). If the FED continues to raise rates, the currencies of the region will probably weaken. Also, the exchange rate will depend on whether the global economy will effectively decelerate in a controlled manner.

Monetary policy and inflation

One of the aspects that seems to be controlled in the region is inflation. Setting aside, the mega-inflation of Venezuela and the hyperinflation of Argentina, the rest of the Latin American countries seem to be in harmony with this driving indicator, for the stimulation of domestic demand, as an engine of economic growth.

The OECD official pointed out that the situation of Argentina is far from the reality of its neighbors, since it does not have an objective inflation policy: "Now the challenge of this country will be how to maintain monetary stability, while it needs to generate greater economic growth."

The experts, that were consulted, agree that the central banks of countries such as Chile, Brazil, and Colombia could enter into a cycle of increase in intervention rates. To the extent that economies are recovering from low growth, banks are likely to start moderating the monetary stimulus, added the Analyst at SURA Asset Management.

On this matter, the Fitch Ratings Analyst also concluded that it is likely that these countries will increase their rates more slowly than expected, given a somewhat weaker external scenario, and with the main economies decelerating."

This article is prepared by the Valora Analitik team for Grupo SURA. Its content is journalistic and does not compromise specific positions or recommendations of our Organization.